Debt is often spoken about in numbers, how much is owed, how high is the interest, and how long it will take to repay. But for many Indians, it is beyond just a financial burden, it’s an emotional and mental one too. A burden that further shapes daily life and traps individuals into a loop of constant borrowing and repaying.

In this blog, we explore the psychological patterns that pull people into debt traps and the emotional cycles that keep them there, while also looking at practical, compassionate ways to regain control and build a healthier relationship with money.

Table of Contents

Understanding the psychological anatomy of the debt-trap:

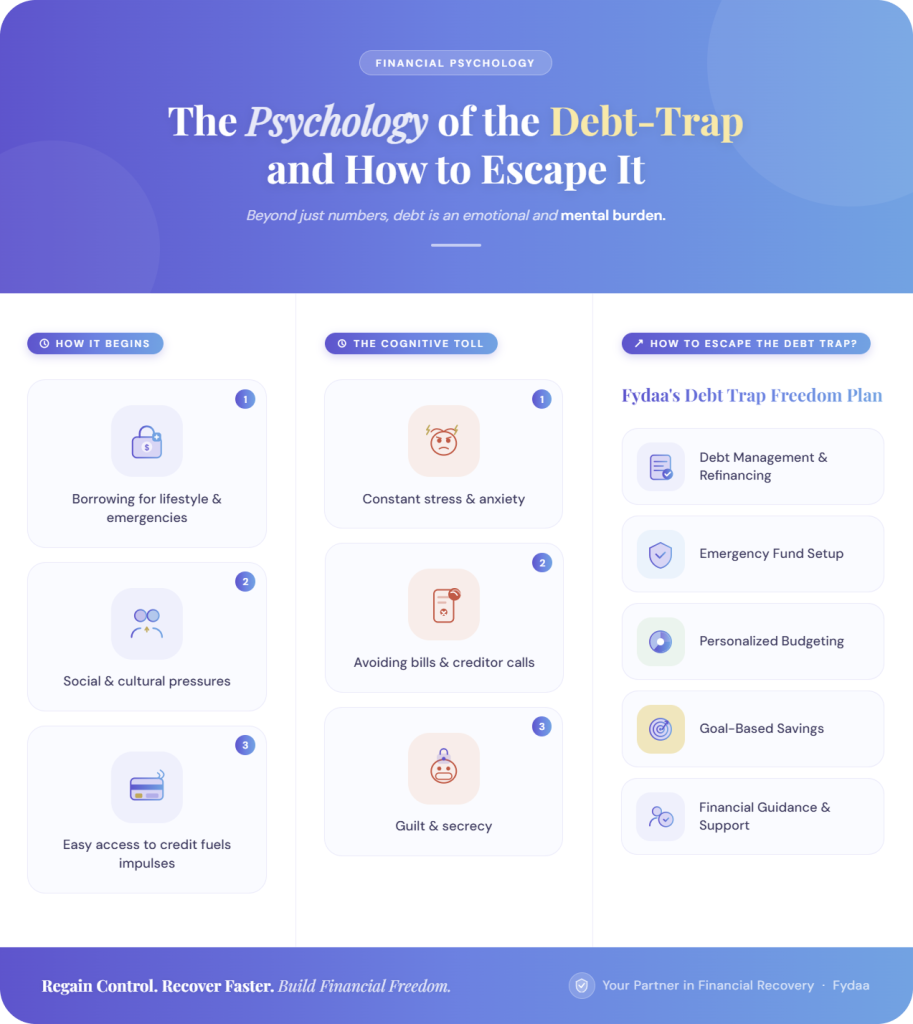

How it begins:

People often borrow to meet lifestyle aspirations or to manage unexpected emergencies. In India, borrowing is frequently shaped by strong social and cultural expectations, where expenses related to weddings, higher education, or religious and family events are seen not just as personal choices but as responsibilities that must be fulfilled. Social pressure and the fear of missing out further push many individuals toward impulsive borrowing, especially when they compare their lives and milestones with those of others. Easy access to credit through loans, credit cards, and digital lending platforms makes borrowing feel safer and more manageable than it truly is. Combined with emergency expenses, overconfidence in future income, and the desire for instant rewards or relief, these factors often become the early drivers that pull individuals into a debt trap before they fully realize its long-term impact.

The Cognitive Toll:

- Managing multiple debts increases mental stress and overloads a person’s decision-making ability.

- Constant reminders, due dates, and repayments drain emotional and mental energy.

- People start focusing only on immediate relief, like paying the minimum amount due, instead of long-term financial health.

- Psychological pressure leads to avoidance behaviors such as ignoring bills or delaying conversations with creditors.

- In India, debt is often linked with guilt and secrecy, so many individuals hesitate to seek help.

- What starts as a financial issue gradually becomes a mental and emotional burden.

- Escaping a debt trap needs more than money; it requires financial awareness and compassionate, trusted guidance.

Finally, how do you really escape the debt trap?

Debt traps, at their core, are often the result of weak or absent financial planning. They grow when essentials like budgeting, building an emergency fund, disciplined saving, expense management, and timely refinancing are overlooked or delayed. Without these foundations in place, even small financial shocks can push individuals deeper into cycles of borrowing and repayment. Gaining control over these areas can significantly reduce financial stress and help people move toward stability and independence.

At Fydaa, the Debt Trap Freedom Plan is designed to address these challenges through personalized and practical guidance. It supports individuals with structured debt management and refinancing solutions, helps set up and maintain an emergency fund, and creates customized budgeting frameworks tailored to their income and lifestyle. Alongside this, the plan encourages goal-based and disciplined savings habits, ensuring that financial decisions are aligned with long-term needs rather than short-term pressure. By combining financial structure with behavioral awareness, the program empowers individuals not only to escape existing debt traps but also to build resilience against falling into them again.

DISCLAIMER: Multistrato Capital Advisors Private Limited Type of Registration: Non-Individual. RIA Registration Number: INA000015969 Validity: Perpetual Registered Office Address: #903, EcoStar Building Off Aarey Road, Vishweshwar Road, Goregaon East Mumbai- 400063, India GST number: 27AAHCM9321Q1ZS

SEBI regional/local address SEBI Bhavan BKC, Plot No.C4-A, ‘G’ Block, Bandra-Kurla Complex, Bandra (East), Mumbai — 400051, Maharashtra Email: sebi@sebi.gov.in

Registration granted by SEBI, membership of BASL and certification from NISM in no way guarantee performance of the intermediary or provide any assurance of returns to investors.

“Investment insecurities market are subject to market risks. Read all the related documents carefully before investing.”