For decades, retirement planning in India has relied on familiarity such as EPFs, fixed deposits and the assumption that family support will always be there. While these methods offer a sense of comfort, they often fall short of meeting the real financial demands of longer life expectancy, rising health-care costs, and inflation. Global retirement readiness indexes consistently place India near bottom, pointing to serious gaps in both coverage, and adequacy of retirement savings.

Recent surveys from 2025- 2026, reveal a growing mismatch between awareness and action.

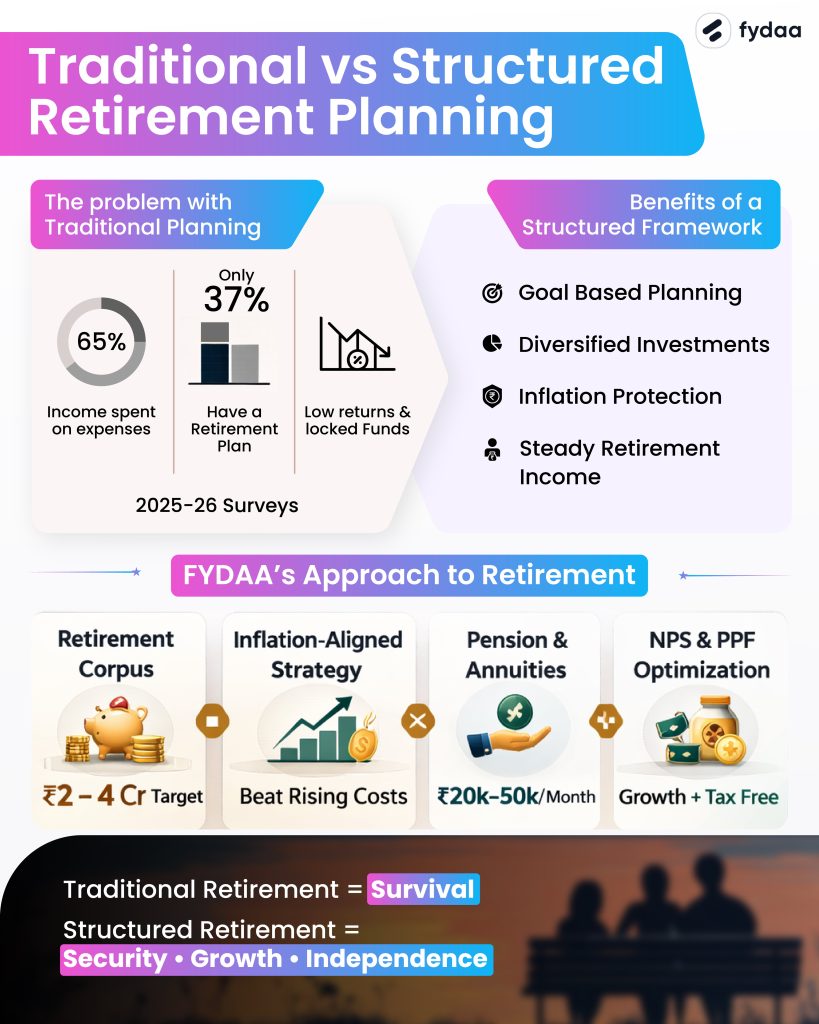

Despite the growing understanding of the importance of planning for retirement, a large share of household income (up to 65%) is still spent on day-to-day expenses. Leaving little room for retirement savings. Consequently, only 37% of people have a structured retirement plan in place. Which poses an important question:

Does the traditional retirement plan really work for Indians?

In this blog, we will discuss the importance of a structured retirement framework, and how it is more effective as opposed to traditional retirement plans.

Table of Contents

What are the drawbacks of Traditional Retirement Planning:

- EPF and PPF usually give returns of around 7-8.5%, which barely keeps up with everyday inflation (6-8%) and falls far behind healthcare inflation (10-12%). Over 25-30 years, this slowly eats into the real value of your retirement savings.

- Since most retirement money is kept only in fixed-income options like EPF and FDs, the growth after inflation is almost zero. In comparison, equity investments have the potential to grow at 10-12% over the long term, helping money actually multiply.

- EPF money is mostly locked in till the age of 58-60, and early withdrawals come with rules and penalties.

PPF has a 15-year lock-in, which means your money is not easily available when you need it urgently. - Many people end up using EPF for big expenses like house purchase or medical emergencies. While this feels necessary at the time, it reduces the money meant for retirement and weakens long-term growth.

- EPF mainly benefits only 6-7% of India’s formal salaried workforce. More than 90% of workers in the informal sector don’t have any structured pension system at all.

- Because of this gap, most people depend on family support after retirement. But with nuclear families becoming common, this safety net is slowly disappearing.

- The government pension under EPS-95 is very small, usually between ₹1,000 and ₹7,500 per month, which is nowhere near enough to manage living costs in cities.

Shortly, traditional retirement tools provide safety, but not enough growth, flexibility, or coverage. On their own, they are no longer sufficient to support a comfortable and independent retirement.

How is a structured retirement framework different?

- A structured retirement framework works better than traditional methods because it is built around your personal goals, not just generic products like EPF or FDs.

- It spreads money across different types of investments instead of relying only on fixed-income options. This helps the retirement corpus grow and survive over 25-30 years, even with India’s 6-8% inflation and rising healthcare costs.

- Unlike rigid plans, it is flexible and regularly adjusted based on life changes, income, and market conditions, so your plan stays relevant over time.

- Tools like retirement corpus calculators help estimate how much money you will actually need, instead of guessing or under-saving.

- Inflation-linked SWPs (Systematic Withdrawal Plans) allow retirees to take out money in a steady and planned way, ensuring monthly income without exhausting savings too early.

- This approach helps people become financially self-sufficient, rather than depending heavily on their children or family for support.

- By planning properly, it reduces the risk of 70% dependency on family, which is becoming unreliable as nuclear families grow.

In short:

A structured retirement framework is not just about saving money, it is about creating a smart, flexible system that protects your lifestyle and independence throughout retirement.

Fydaa and Structured retirement plan:

- Retirement corpus calculation:

Instead of guessing how much money will be needed, custom tools like Excel models and simulations are used to calculate a realistic retirement corpus. These consider your age, income, and lifestyle. For example, a middle-class family in Mumbai may need around ₹2-4 crore in today’s value, which is roughly 250-300 times their monthly expenses. - Inflation-adjusted planning:

The plan is tested against different inflation scenarios, especially higher healthcare inflation which is around 6-12%. SIP amounts are increased gradually every year so that savings keep pace with rising costs, unlike fixed deposits, which stay static and lose value over time. - Pension and annuity options:

Guidance is provided on using EPS and NPS annuities to create a guaranteed monthly income after retirement. Private pension plans are also explored to improve income beyond the low limits offered by EPS alone.

NPS and PPF strategy:

NPS is structured with a higher equity portion (up to 75%) for long-term growth, while PPF is used as a stable, tax-free debt base.

Voluntary Provident Fund (VPF) contributions can be added on top of EPF to make better use of available limits and strengthen retirement savings

In simple terms:

This approach combines smart calculation, inflation protection, and multiple income sources to build a stronger and more reliable retirement plan than traditional methods alone.

Retirement planning today needs more than basic savings and guesswork. A registered investment adviser helps you create a clear, personalized plan based on your goals, income, and future needs. With professional guidance, your money is invested wisely, adjusted over time, and protected against inflation and rising expenses. This support turns retirement planning into a structured journey, giving you confidence, stability, and true financial independence in the years ahead.

To Know more, click here

DISCLAIMER: Multistrato Capital Advisors Private Limited Type of Registration: Non-Individual. RIA Registration Number: INA000015969 Validity: Perpetual Registered Office Address: #903, EcoStar Building Off Aarey Road, Vishweshwar Road, Goregaon East Mumbai- 400063, India GST number: 27AAHCM9321Q1ZS

SEBI regional/local address SEBI Bhavan BKC, Plot No.C4-A, ‘G’ Block, Bandra-Kurla Complex, Bandra (East), Mumbai — 400051, Maharashtra Email: sebi@sebi.gov.in

Registration granted by SEBI, membership of BASL and certification from NISM in no way guarantee performance of the intermediary or provide any assurance of returns to investors.

“Investment insecurities market are subject to market risks. Read all the related documents carefully before investing.”